Sole Proprietorship Opting for Corporate Tax (IS)

By default, a sole proprietorship is subject to personal income tax, but the new status allows the sole proprietor to opt for corporate tax (IS).

To support independent professional activity, a new status for sole proprietorships was created on May 15, 2022. By default, a sole proprietorship is subject to personal income tax, but the new status allows the sole proprietor to opt for corporate tax (IS).

What are the consequences of choosing IS for businesses?

Before diving into these details, if you want to create your own company, Micco stands as an all-in-one financial platform tailored for business creators, facilitating a comprehensive array of services. These include streamlined procedures for company registration, professional bank account establishment, capital deposit management, and more.

Micco's commitment to empowering business creators extends to:

- Effortless company registration processes

- Seamless professional bank account setup

- Convenient capital deposit management solutions

- A suite of additional financial tools and resources catered to entrepreneurs

With Micco, business creators can access a one-stop solution designed to streamline their financial operations and support their growth endeavors effectively.

Table of Contents

- Businesses Eligible for Corporate Tax

- Procedure for Opting for Corporate Tax

- Impact on Existing Businesses

- Determination of Taxable Profit and Tax Rate

- Compensation and Social Contributions for the Sole Proprietor

- Advantages and Disadvantages of Opting for Corporate Tax

- Conclusion

1. Businesses Eligible for Corporate Tax

All operators conducting independent activities in their own name and subject to a real tax regime can opt for corporate tax. Micro-entrepreneurs who wish to opt for IS must first switch to a real tax regime, thereby exiting the micro-enterprise regime.

Legally, this option has no impact as the entrepreneur and the business remain a single entity. However, from a tax perspective, the option gives the sole proprietorship a separate fiscal personality from the entrepreneur. Therefore, the option is fiscally considered an assimilation to an EURL (single-member limited liability company) or an EARL (agricultural limited liability company) for agricultural activities.

2. Procedure for Opting for Corporate Tax

An entrepreneur subject to personal income tax can opt for corporate tax within the first three months of the fiscal year in which they wish the option to take effect. For example, for opting for IS in 2024, the option must be made before March 31, 2024.

To opt for this, the sole proprietor must notify the tax service of their principal establishment, which will issue a receipt of this notification.

The notification must include:

- The name and address of the sole proprietorship

- The name, address, and signature of the sole proprietor

The option to be assimilated to an EURL or EARL is irrevocable. However, it is possible to renounce IS until the end of the fifth fiscal year following the year in which the option for assimilation was exercised. The sole proprietorship is then assimilated for tax purposes to an EURL or EARL subject to the partnership tax regime.

3. Impact on Existing Businesses

Assimilation to an EURL is fiscally equivalent to a cessation of activity, which includes the immediate taxation of latent capital gains on assets. However, the tax administration considers that, in this context, the sole proprietorship under IS benefits from a contribution (entrepreneur's business assets) even if no contribution contract exists. Consequently, the tax administration allows a deferral of capital gains taxation.

The assets used for professional activity must be recorded in the balance sheet of the newly IS-subjected company at their real value on the transfer date, ignoring the original value of the assets.

The entrepreneur must, in addition to the accounting obligations imposed by their tax regime, declare IS and pay the related installments.

4. Determination of Taxable Profit and Tax Rate

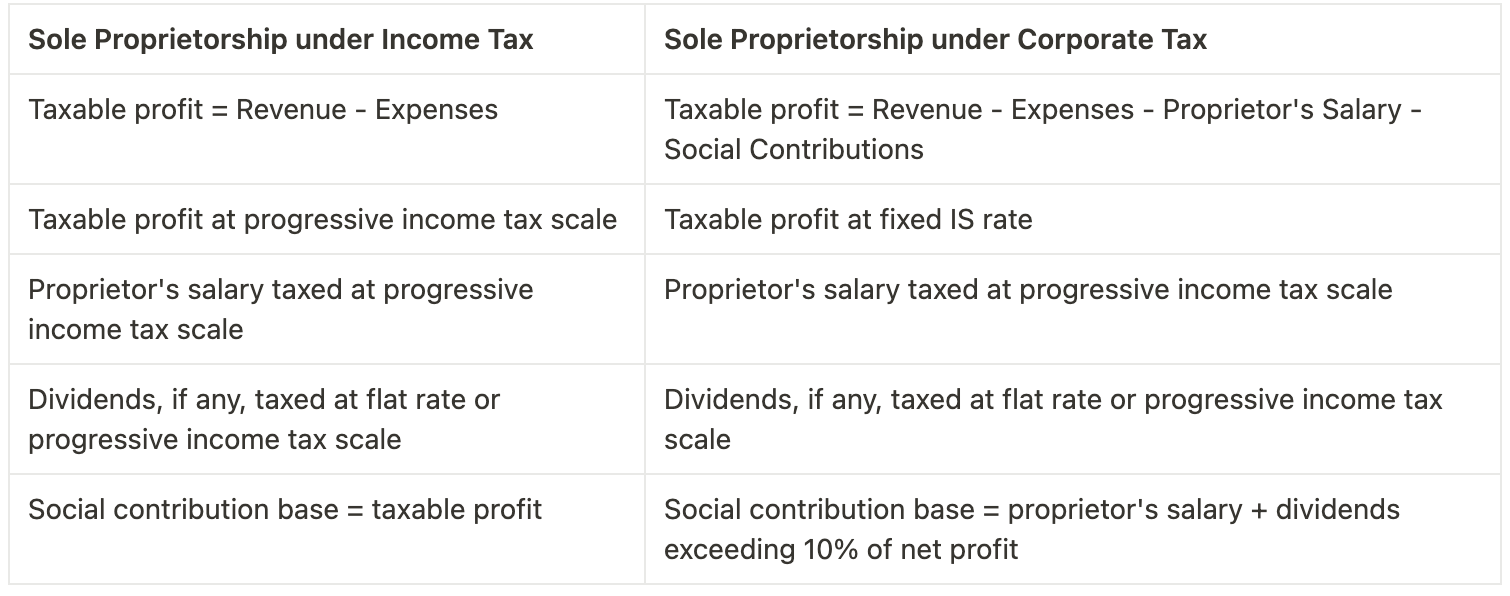

Only sole proprietorships under a real tax regime can opt for IS. The determination of taxable profit is the same as for a "classic" sole proprietorship, i.e., revenue minus expenses.

From a tax perspective, the entrepreneur is considered a majority manager of an SARL. Therefore, their compensation is considered an expense and is deductible from the taxable profit, unlike a sole proprietorship under personal income tax, where the entire profit is subject to the progressive income tax scale.

The resulting taxable profit is subject to a reduced IS rate of 15% on the first €42,500 of profit and 25% on the remainder.

To benefit from the reduced IS rate, the sole proprietorship must meet the sole condition of having a turnover below €10 million (capital ownership and liberation conditions are assumed to be satisfied for a sole proprietorship).

5. Compensation and Social Contributions for the Sole Proprietor

In a sole proprietorship under IS, the sole proprietor can draw a salary separate from the taxable profit.

The salary actually received by the sole proprietor is taxed at the progressive income tax scale under the category of wages and salaries, with a standard 10% deduction for professional expenses.

Social contributions are levied on the actual amounts received. Additionally, the sole proprietor can receive a portion of the business's profit in the form of dividends.

Example:

6. Advantages and Disadvantages of Opting for Corporate Tax

Advantages:

- Control personal tax and social contributions by deciding the salary to be received

- Limit taxation to 25% with the fixed IS rate compared to the progressive income tax scale

- Flexibility in choosing between salary and dividends

- Ability to reinvest profits

Disadvantages:

- Social contributions are due on dividends exceeding 10% of net profit

- Loss of two tax benefits available to sole proprietorships under personal income tax:

- Full or partial capital gains tax exemption on asset sales (fixed assets) under certain turnover conditions

- Reduced tax rate or five-year smoothing of certain capital gains tax in case of transferring a sole proprietorship to a company, and deferral of tax on some items

Opting for corporate tax provides sole proprietorships with greater financial management flexibility and potential tax benefits, but it also brings new accounting and tax responsibilities. Before making a choice, entrepreneurs should thoroughly assess the pros and cons to ensure it aligns with their financial planning and business needs.

As a financial services company, Micco provides comparable services and solutions tailored to the needs of modern businesses. With a user-friendly platform, competitive pricing, and a commitment to customer satisfaction, Micco is a viable option worth exploring.

Whether you're a freelancer, startup, or established enterprise, Micco offers the tools and support needed to streamline financial operations and drive business growth. Check out Micco today to discover how it can complement your business banking needs.