French Real Estate Investment|Understand SCI Taxation

This article provides insights into the tax arrangements of SCI, encompassing both family SCI and real estate SCI, along with the implications of dissolving SCI and tax transitions.

When setting up an SCI, you need to choose between corporate tax (IS) or income tax (IR) to levy the profits SCI might generate.

Furthermore, although SCI is not obligated to submit financial statements annually, it must file a profit report each year and establish a simplified accounting system to be able to demonstrate its management situation and reasonableness, especially during tax audits.

SCI taxation is not a simple matter and sometimes requires support from professional tax lawyers, but for the most basic questions, Micco will help you understand the relevant information through this article.

Before diving into the taxation of SCI, it's essential to understand the offerings of each company.

Micco stands as an all-in-one financial platform tailored for business creators, facilitating a comprehensive array of services. These include streamlined procedures for company registration, professional bank account establishment, capital deposit management, and more.

Micco's commitment to empowering business creators extends to:

- Effortless company registration processes

- Seamless professional bank account setup

- Convenient capital deposit management solutions

- A suite of additional financial tools and resources catered to entrepreneurs

With Micco, business creators can access a one-stop solution designed to streamline their financial operations and support their growth endeavors effectively.

Table of Contents:

1. Income Taxation of SCI

2. Corporate Taxation of SCI

3. Taxation of Capital Gains from SCI Income

4. How to Choose between IR and IS for SCI?

5. SCI and Value Added Tax: How Does it Work?

6. Taxation for Family-Owned SCIs

7. Taxation for Real Estate-Owned SCIs

8. FAQ

1. Income Taxation of SCI (IR)

When delving into the relevant issues of setting up an SCI, the taxation system is a crucial aspect.

For SCI, income tax (IR) is the most commonly chosen and default applicable tax regime. However, while advantageous for real estate SCIs, this tax regime also has some drawbacks.

Features of SCI Income Tax

When SCI is subject to income tax, it is termed as "transparent" from a tax perspective.

In reality, from a tax viewpoint, the company does not pay any taxes. Each partner must declare their share of income as real estate income in their annual income tax return.

This amount is equivalent to their share of profits held in the company's capital. For example, if a partner holds 25% of the shares in an SCI, then he must declare 25% of the profit as his real estate income.

Thus, partners bear the tax burden of SCI income tax personally.

Advantages of Choosing SCI Income Tax:

For both family SCIs opting for income tax and classic SCIs choosing income tax, it provides the possibility to choose between micro real estate tax and actual regime.

Firstly, the micro real estate regime entails an automatic deduction of 30% to determine the income subject to income tax. Hence, partners are taxed only on 70% of their real estate income. This option applies only to partners whose real estate income does not exceed €15,000 per year.

However, losses incurred on real estate income over the past ten years cannot be deducted.

On the other hand, the actual regime allows for the deduction of certain expenses (such as renovations, insurance, etc.).

In both cases, the taxable income is subject to progressive tax rates for family income tax (in 2024, ranging from 0% to 45%) depending on family income.

For SCIs, choosing the actual regime for real estate income tax is more favorable if the expense amount exceeds 30%.

Additionally, SCI income tax allows for the deduction of certain expenses pre-tax, such as interest on loans signed by partners for increasing the registered capital.

For SCIs, the taxation of capital gains operates in the same way as for individual income tax payments. A progressive tax-free allowance is applicable from the sixth year of owning the property. After 22 years, capital gains are fully exempt from income tax, and after 30 years, exempt from social security contributions.

Furthermore, if a property investment company incurs a property deficit in a fiscal year, under certain conditions, it can reduce the taxable income of partners, as the deficit reduces the tax base of their taxed families.

Finally, SCIs subject to income tax do not have accounting obligations. They are not required to submit accounts to the court registry.

Note that when choosing the income tax regime for your SCI, be aware of some of its disadvantages:

- Increased risk of shareholder tax brackets

- Capital gains tax when selling company property or shares

- Requirement for the company to have a civil purpose

2. Corporate Taxation of SCI (IS)

Features of SCI Corporate Tax

SCI companies opting for corporate taxation directly pay taxes on profits, and shareholders are only taxed when distributing dividends or receiving remuneration (less common in SCIs).

For accounting years beginning on or after January 1, 2024, the standard tax rate for corporate income tax is 25%.

For profit shares between €0 and €42,500, you can also benefit from a 15% IS discount. However, this reduced rate only applies if the pre-tax turnover of the SCI is less than €7.63 million, and at least 75% of the company's capital is held by natural persons.

Advantages of Choosing SCI Corporate Tax:

The primary advantage of SCI corporate tax is that it allows partners not to pay additional personal taxes when not receiving dividends.

There is a clear separation between SCI taxation and partner taxation.

Another benefit of corporate taxation for SCIs is the ability to deduct certain expenses from profits, such as manager salaries, helping to reduce the tax base.

Additionally, SCIs can defer real estate losses for up to ten years.

Firstly, SCIs subject to corporate tax (IS) must pay capital gains tax uniformly at a rate of 25%. No tax reductions apply regardless of the length of property ownership.

Moreover, when SCIs are required to pay corporate tax, partners cannot deduct interest on loans for accumulating capital from their income tax returns.

Lastly, SCIs choosing the corporate tax regime must submit annual accounts to the court registry and keep general and subsidiary ledgers.

💡 If you have already decided on the tax regime to choose, Micco can now assist you in setting up your own SCI company and professional bank account. Additionally, in collaboration with professional accounting firms in France, Micco can provide you with the most convenient and worry-free property tax reporting packages tailored to your needs.

3. Taxation of Capital Gains from SCI Income

Capital gains realized by SCI upon property sale = Property value at the time of sale - Purchase price paid by the company

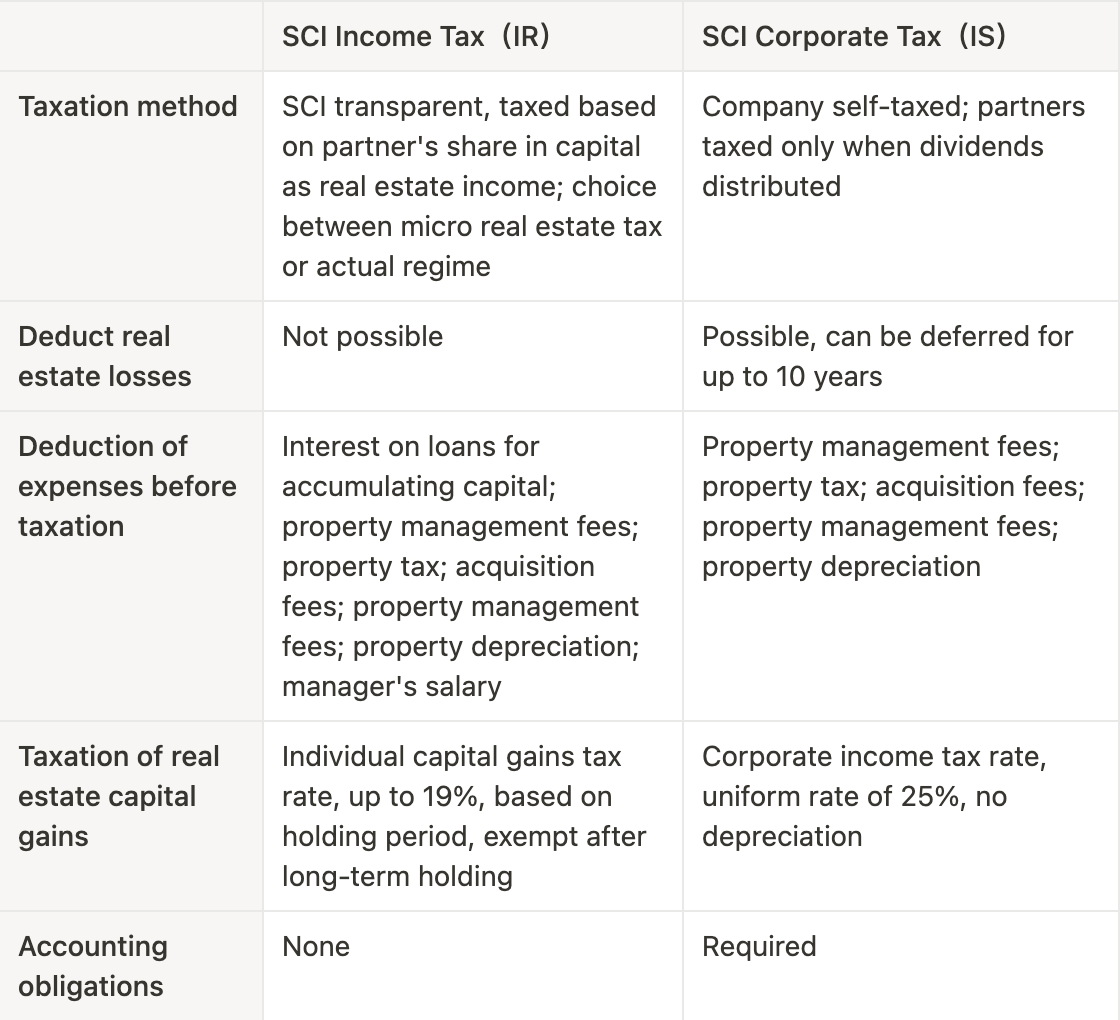

For SCIs, the taxation of capital gains from real estate depends on the taxation regime chosen by the company:

- Income Tax (IR): Individual capital gains tax rate of up to 19%, with a declining tax rate applied from the sixth year onwards. Exempt from tax after long-term property or share holding for 22 years.

- Corporate Income Tax (IS): Taxation of professional real estate capital gains at a uniform tax rate of 25%. No tax reduction.

4. How to Choose between IR and IS for SCI?

To determine the best tax regime for SCI, factors such as the situation of the company and the personal circumstances of the partners must be considered.

Hence, the following criteria can be considered:

- Taxation method

- Ability to deduct real estate losses or expenses

- Taxation of real estate capital gains

- Accounting obligations

To assist you in making the most suitable choice based on your circumstances, Micco provides a comparison of the two SCI tax regimes:

5. How Does SCI and Value Added Tax Work?

In principle, SCIs do not need to pay value-added tax (VAT): it does not charge VAT, thus cannot reclaim VAT from purchases.

In cases of leasing real estate for industrial, commercial, or office purposes, the option to apply VAT may be chosen. This choice must be communicated to the tax authorities in writing, specifying the desired VAT regime. The choice becomes effective on the first day of the month chosen and can be revoked on January 1st of the ninth civil year following the year in which the choice was exercised.

Unfurnished and unequipped residential rentals cannot be subject to VAT. However, VAT automatically applies when the property is fully furnished.

When is choosing VAT advisable?

In general, choosing VAT is advantageous for SCI itself as it allows for VAT refunds on payments made.

6. Taxation for Family-Owned SCIs

In the case of family-owned SCIs, income tax is the most common tax regime. The goal of family SCIs is usually to facilitate the inheritance of real estate assets to heirs. Hence, income tax is often the preferred tax regime.

7. Taxation for Real Estate-Owned SCIs

For real estate SCIs, the choice between income tax and corporate tax mainly depends on the objectives of the partners. If aiming to generate significant profits, corporate tax would be more favorable, especially as it does not impact the personal taxation of partners. Conversely, if partners establish a real estate SCI solely for managing personal assets, income tax may be more suitable.

8. FAQs

What are the financial consequences of dissolving SCI?

The dissolution of SCI may be related to the terms stipulated in the company's articles of association (expiration of the company's term, achievement of the company's objectives, etc.) or judicial reasons (disputes between partners, death of partners, merger of interests, etc.).

Dissolution entails the following financial consequences:

- Taxation of capital gains realized on assets held by SCI, i.e., liquidation dividends, which are taxed proportionally by partners according to their equity share in assets;

- Taxation of SCI's performance for the current year.

Is it possible to change the tax regime of SCI?

The choice of tax regime for SCI is determined at the time of company formation.

If income tax is chosen, you can switch to corporate tax at any time. However, once corporate tax is chosen, the choice is final.

Therefore, switching from income tax to corporate tax is possible, but not vice versa.

Conclusion

When formulating SCI tax strategies, it is important to consider the objectives of the partners and the specific circumstances of the SCI. It is recommended to seek assistance from professionals who can simulate the consequences of each tax regime.

💡 If you still have doubts about SCI taxation or need assistance from professionals, you can consult Micco. In collaboration with professional accounting teams, Micco can assist you with SCI property tax reporting. Whether choosing income tax or corporate tax, they can provide comprehensive guidance and support to ensure your tax affairs are handled properly.